Welcome back to the real estate private equity case study series where we focus on the public REIT valuation of Aimco. Right now we’re building a net asset value (NAV) analysis, and in the last posts we knocked out gross asset value (GAV) and spoke to consolidation. This post will shift to focus on the other half of our NAV: the debt. As with gross asset value, let’s take another look at the 2Q20 balance sheet and run through the lines we care about most. Pay close attention, because this sort of public analysis is common in real estate investment case studies!

Liabilities

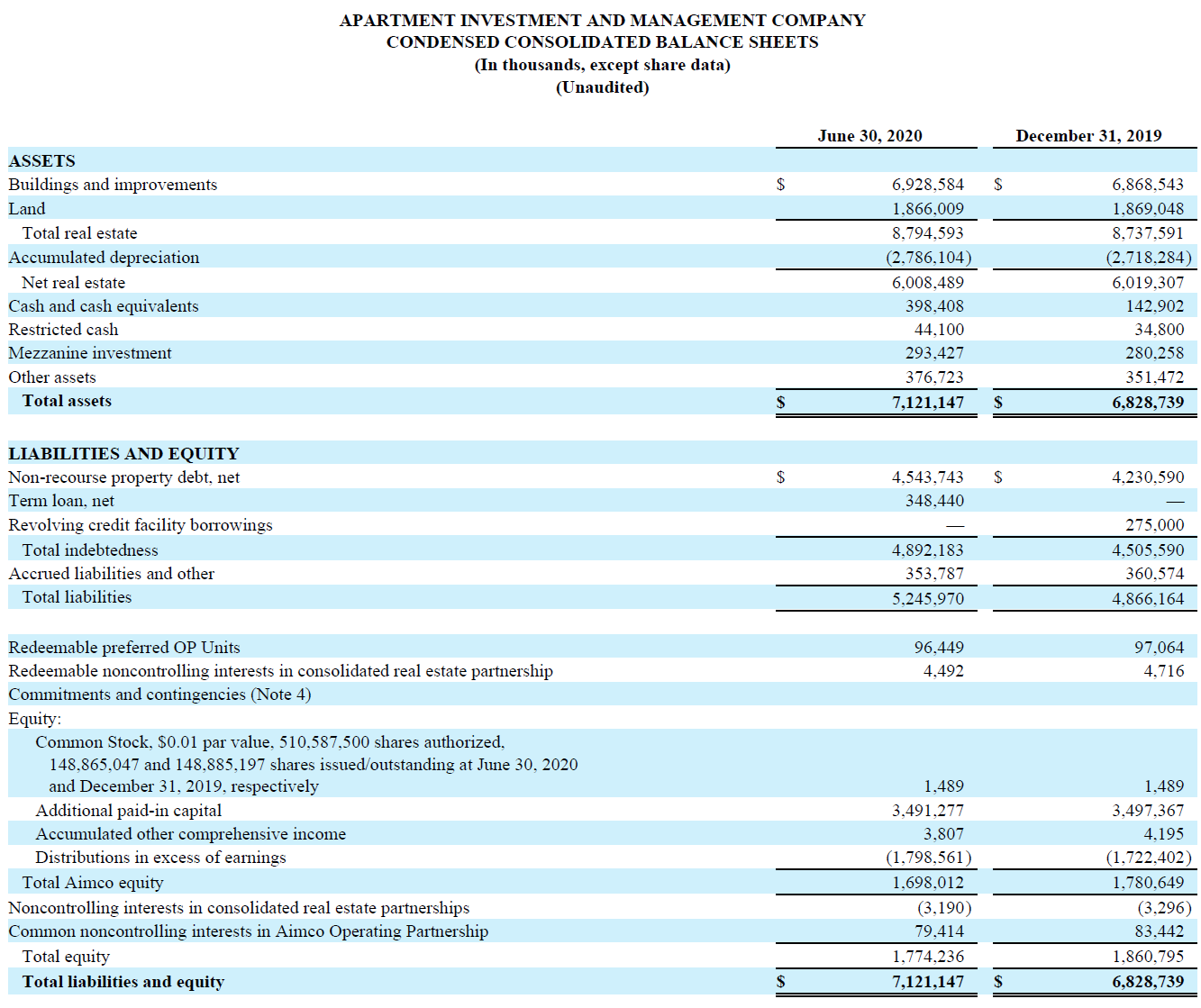

Balance sheets are great because they give us a 10,000 foot snapshot of the most relevant items for our NAV analysis. As you see above, Aimco primarily leverages itself with non-recourse property debt, but it also has a term loan, a revolving credit facility, and some other accrued liabilities. All said, their capital structure is pretty straightforward compared to some peers.

Non-Recourse Property Debt, Net

AIV has $4.5B of non-recourse property debt, net. Let’s unpack some of those keywords:

- Property Debt: The debt is secured by the properties. This means that the property debtholders are first in line in the capital stack. In Aimco’s specific case, the property debt gets paid before the corporate term loan, revolver, redeemable preferred OP units, and the equity.

- Non-Recourse: If the property defaults, the property debtholders have no recourse to other assets the company owns. For example, if I issue AIV a non-recourse loan for property A, and three years later property A goes bankrupt, I can only lay claim to the value of property A. I can’t go after any other properties that Aimco owns, or any of Aimco’s balance sheet cash. All else equal, non-recourse property debt is favorable to Aimco when compared against recourse property debt, which would be allowed to seek recompense elsewhere from Aimco’s balance sheet. Of course, the added risk to the lender of non-recourse debt is factored into the cost of the debt.

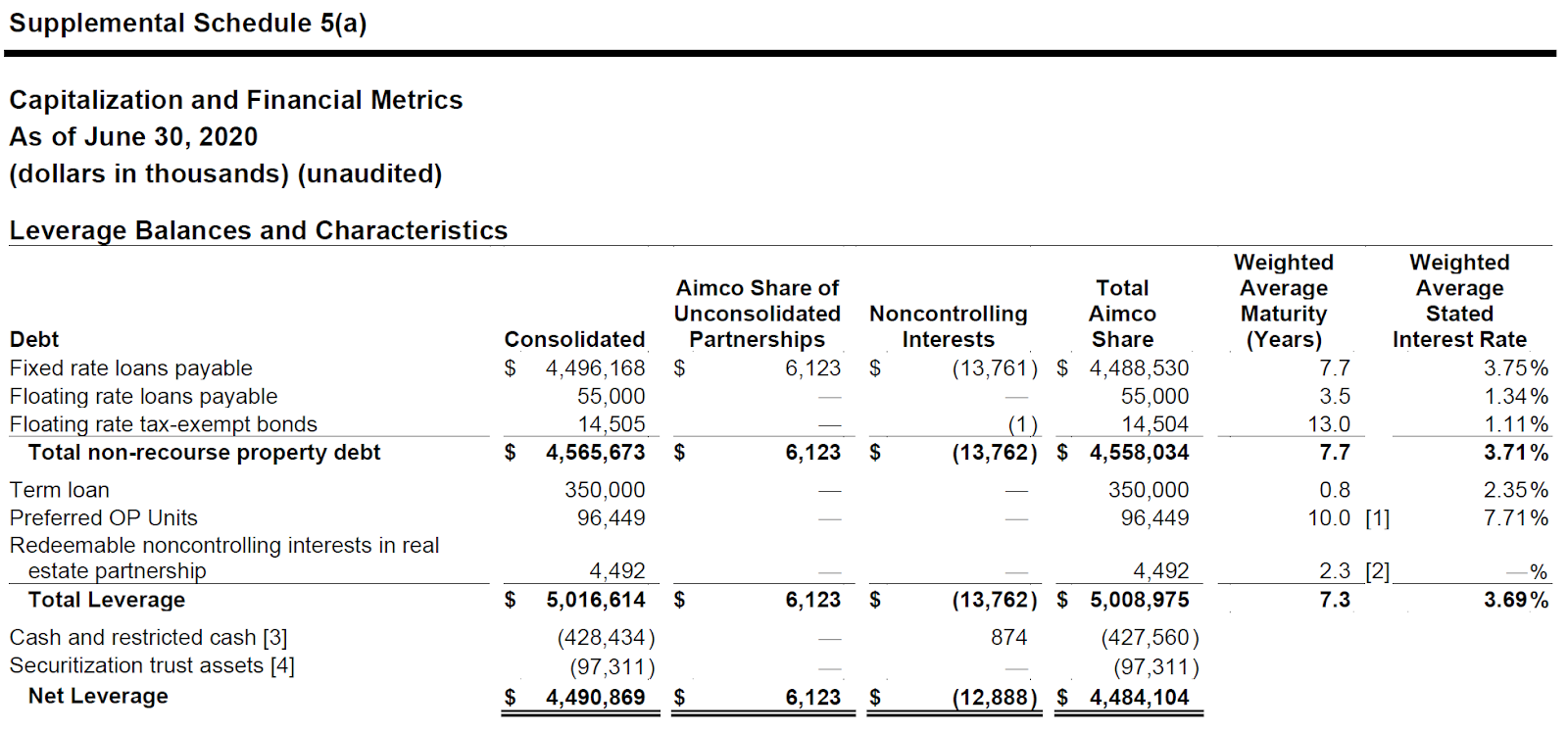

- Net: This net means net after issuance costs. But when we pull the property debt balance into the NAV, we actually want to have the figure gross before issuance costs. We can find the gross consolidated balance on Aimco’s 2Q20 financial supplemental schedule 5(a), below. The gross balance of $4.566B against the net balance of $4.544B implies $22M of issuance costs. Yet when the debt comes due, we will still owe the full gross balance, so we ignore the net figure and always look for the gross figure when building an NAV.

Where to Find Property Debt

Ideally, Aimco would publicly report its property debt on an asset-level basis. That way, we could map each piece of debt to each property shown in the asset list. Unfortunately, the figures in Aimco’s balance sheet are pretty high-level. The best public detail on debt can typically be found either in the footnotes of the major public filings, or somewhere in the company’s supplemental. As mentioned in the bullet on Net above, I’m going to pull in Aimco’s consolidated debt balances from pdf20/doc19 of its 2Q20 Supp.

Term Loan and Revolving Credit Facility

Below the property debt balance of $4.565B, we also see that Aimco has a $350M term loan. In terms of seniority (which you can read more about here), corporate term loans come after property-level debt. This is simply because the property-level debts have specific properties they get first dibs on, whereas the term loan gets dibs on the residual value that is unencumbered by the property debt before it. Thus, term loans carry a higher rate of interest than the property-level debt.

If we scroll through the filings, we’ll land on doc17 which tells us this term loan was issued quite recently, on April 20, 2020. The purpose of the term loan was to pay down its revolving credit facility, which currently sits at zero (think of an RCF as a corporate credit card). The term loan itself matures in April 2021 but it has a one-year extension option, which means it effectively matures on April 2022 since the company can kick out the maturity by one year, assuming they maintain compliance with their financial covenants. The term loan bears an interest rate of L+1.85%, which we’ll include in our model.

Conclusion

That wraps up our discussion on debt. In the next post, we’ll focus on handling the remaining items such as the Redeemable Preferred OP Units, noncontrolling interests, and fully-diluted share count. At the bottom of this post, I have copied the current status of our NAV build updated for the notes above, which remains as a work-in-progress.

Learn with Leveraged Breakdowns

Leveraged Breakdowns is the premier resource for real estate private equity case study prep. Our content is exclusively produced by megafund investors who are keen on helping outsiders break into this exclusive industry. We offer a suite of helpful products, including an extensive real estate private equity interview guide as well as downloadable, follow-along real estate investment case studies. In fact, active subscribers can download the model used in this very post!

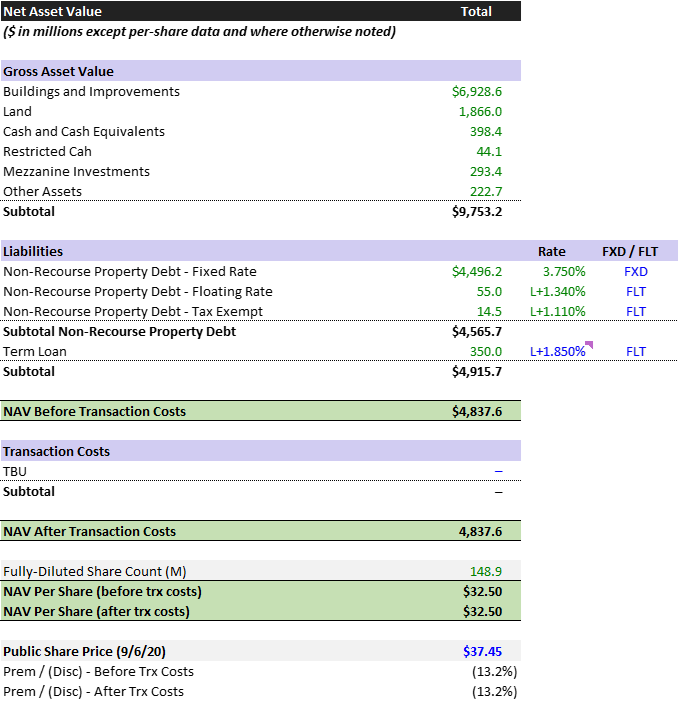

Current NAV Build